The fifth of the Ten Rules of Investing For Beginners is: don’t attempt market timing. Focus on Time in The Market, not Market Timing. You can’t outsmart the market. Nobody can. The strong warning to not try to time the market applies to the bond market as well as the stock market—it’s a loser’s game.

Next steps:

- Watch next video in this series: Rule #6: Use index funds when possible.

- Download cheat sheet Ten Simple Rules to Common Sense Investing,

a printable 1-page PDF summarizes Boglehead Investing. - Take a free course: Common Sense Investing,

or Where Should I Put Money?

Read the transcript—because you will be tempted to Time The Market. Focus on Time In The Market.

Imagine this: You’ve invested in a stock, or a fund, and its value has plummeted to half of what it was worth a year ago, with no end in sight. You hate to lose money! Should you sell to prevent further loss?

Or, perhaps the market’s been rising and you are wondering whether you are missing the boat and should be owning the current winner?

Investing is simple—but not easy.

— Unknown

These are examples of trying to beat the market using timing. It’s a loser’s game. It is at least very difficult, if not impossible, to succeed at market timing over the long-run.

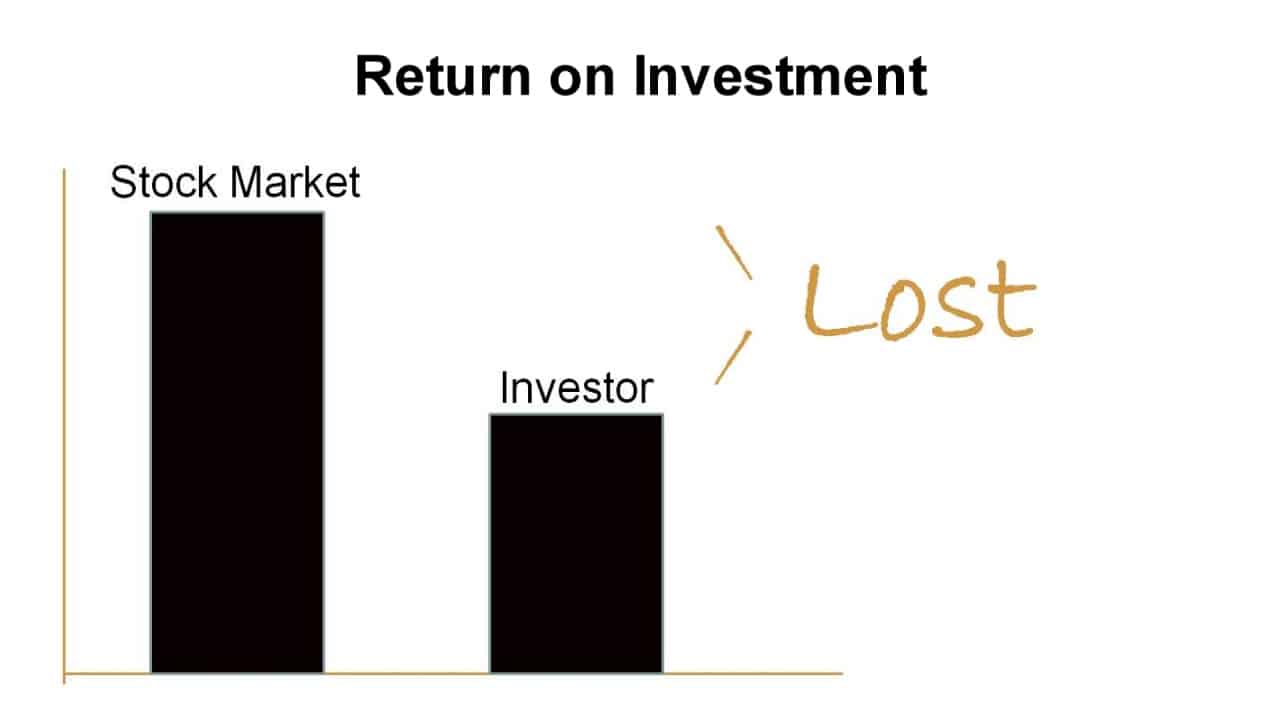

It turns out that investor money flows into stock funds after good performance, and goes out when bad performance follows. Investors chasing performance are always too late.

For a recent 25 year period, John Bogle found that the vast majority of investors earned 5% less than the overall stock market return. Over half of this gap was from market timing; the rest unnecessary costs.1

It’s simple to achieve the market return because you can buy a single mutual fund that owns all publically held companies for a low cost. But, it’s only easy if you have a plan that matches your ability, willingness, and need to take risk, then you stick to it and weather all the sales efforts that are targeted at you.

To make money from stocks and bonds, it is important to acknowledge that you are investing in companies, either by becoming a lender to them, through holding a company’s bond, or by becoming a partner with them, through buying a company’s stock. We, collectively, buy and hold these shares for the long term, sharing the wealth all these companies generate thru their growth, resourcefulness, and innovation. And we, collectively, all earn the market return.

But within this pool of shareholders, there is short term trading between investors. And for every person that beats the market return, there is an equal and opposite loser. The huge financial services industry is very adept at convincing you that they can help you get better returns than the market so that you’ll watch their channel, purchase their newsletter, or invest in their fund.

My next video will help you distinguish a good fund from a lousy one.

Attempting to predict the future direction of the market is only the first of the two common timing mistakes.

It’s also incredibly tempting to invest in the most recent top performing categories of stocks and bonds. Last year, the best performing investments were the category of stocks known as small cap growth, followed by real estate companies, and so forth down to international stocks, and finally bonds.2 Predictions here are futile. Here’s where last year’s top performer was in previous years. Here’s where last year’s second best category was in previous years. You get the idea. John Bogle warns, “Don’t think you know more than the market. Nobody does.”

Don’t think you know more than the market. Nobody does.

John C. Bogle

The other common mistake is to invest in yesterday’s top performers. Winning strategies buy and hold a portion of all of the nation’s publicly held businesses at a very low cost. By doing so you are guaranteed to capture almost the entire return that they generate in the form of dividends and earnings growth.3

Here’s a short example. Henry is saving for his retirement in 30 years. He chooses to own his age in bonds which means, this year, 35% of his retirement savings are allocated to bonds, and 65% are allocated to a fund that owns the entire stock market. He rebalances every birthday so very gradually his percentage of bonds increases.

Now, does he hesitate after every paycheck and consider whether stocks might be cheaper to buy tomorrow? No. He set-up his purchases to occur automatically, and avoids that first timing mistake.

Does he ever consider which companies (or mutual funds) are doing best this month? Nope, by simply buying a small piece of the whole market he gets to own them all, and avoids that second timing mistake.

How ’bout rebalancing every birthday: is that “market timing”? No again. It’s an example of having a plan and sticking to it.

Find other explanatory videos, smart tips, and links to useful resources at FinancingLife.org.

Related articles:

- Must-read guide: Smart Investing for Beginners

- Video overview of Intro: Ten Rules of Investing for Beginners

- Step 1: Develop a workable plan.

- Step 2: Start saving early.

- Step 3: Choose appropriate investment risk.

- Video overview of Step 4: Diversify.

- Video overview of Step 5: Never try to time the market.

- Video overview of Step 6: Use index funds when possible.

- Video overview of Step 7: Keep costs low.

- Video overview of Step 8: Maximize after-tax returns.

- Video overview of Step 9: Keep it simple.

- Video overview of Step 10: Stay the course.

- Video overview of The ABCs of Common Sense Investing

- Must-read guide: How To Build An All Weather Portfolio With Stocks and Bonds

- Courses at: FinancingLife Academy

Footnotes and Video Production Credits for Rule #5: Focus on time in the market, not market timing.

(1) The stock market index fund was providing an annual return of 12.3 percent and the average equity fund was earning an annual return of 10.0 percent, the average fund investor was earning only 7.3 percent a year. The Little Book of COMMON SENSE INVESTING, by John C. Bogle, 2007, p.51.

(2) http://www.russell.com/us/documents/syndication/value_of_diversification_004000579.pdf

(3) The Little Book of COMMON SENSE INVESTING, by John C. Bogle, 2007, p.xi.

The Behavior Gap picture, and the Buy High Sell Low picture are inspired by Carl Richards’ outstanding collection of sketches at www.behaviorgap.com .

The opening/closing music “Because” is by David Modica from his Stillness and Movement album, published and licensed by www.Magnatune.com.

The closing photo “Trees in the Fog” is by Yann Richard under the terms of the Creative Commons BY 2.5 license.

This video may be freely shared under the terms of this Creative Commons License BY-NC-SA 3.0.

Video copyright 2009-2019 Rick Van Ness. Some rights reserved.

————————————————————————–

What’s your learning style? Would you prefer a book?

- to learn at your own pace?

- to mark with notes?

- to use as reference?

- to give as a gift?

- or, even just to support this non-profit educational website (thanks!)

Take a closer look at the paperback book.

| Common Sense Investing: Ten Simple Rules to Finance Your Dreams

|