Start with a sound lifestyle — your financial lifestyle — where you live below your means. You need to do this in order to save. You need to save before you have anything to invest.

Read The Transcript to Start With Sound Lifestyle

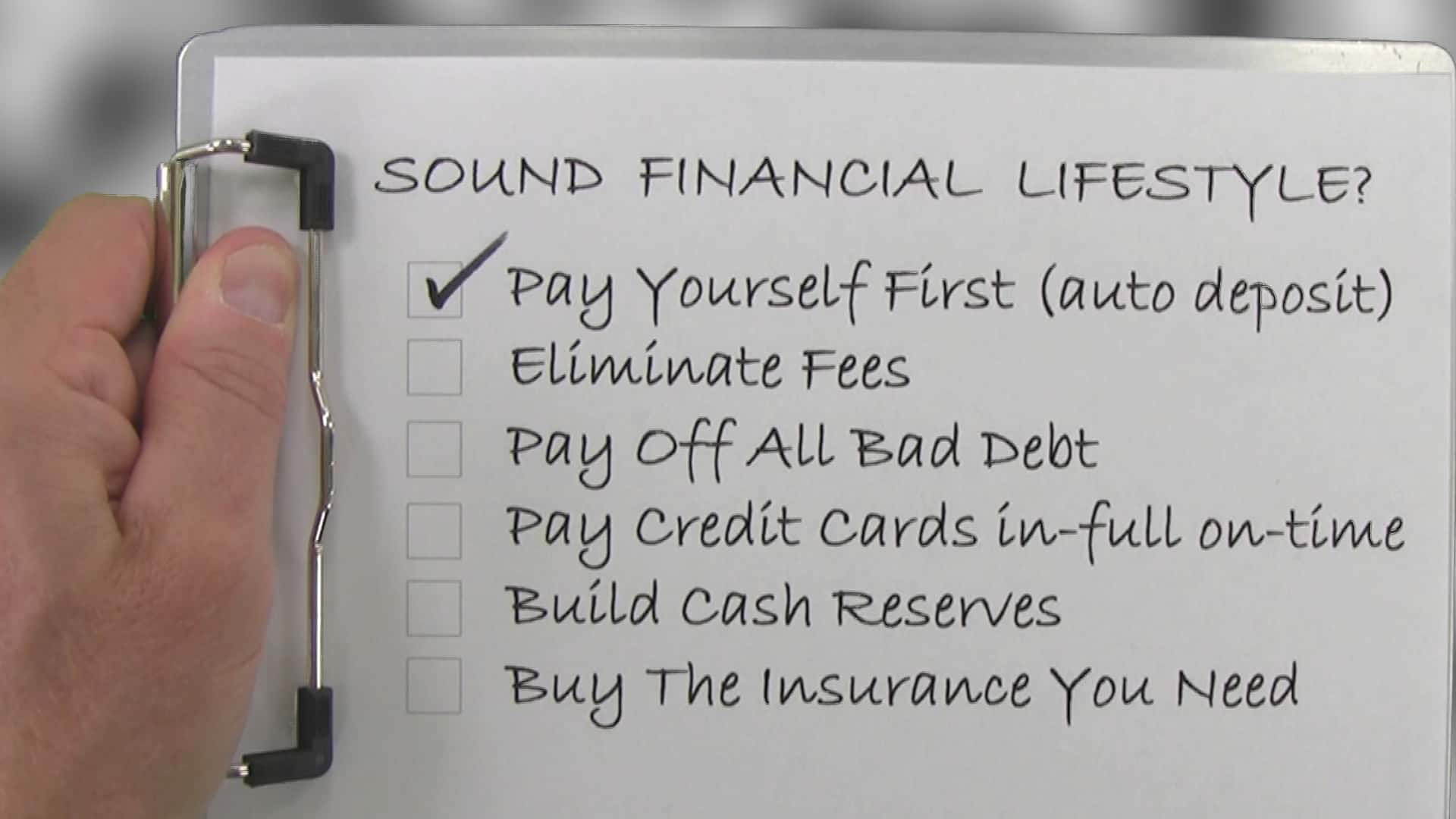

If you haven’t already, you should use the very first money you save to establish a sound financial lifestyle, before investing for your future. This will be our checklist.

Hopefully you are saving money from every paycheck. If you are not saving 15%, save whatever you can. Start from wherever you are.

Some people start with a level they can save monthly and pledge to increase that level with future salary increases until they reach their saving goals. Choose something that will work for you. The most important thing is to start.

The technique of paying yourself first has proven to work for millions. It’s our human nature that we don’t miss it if we don’t see it.

It’s easier to save if you first eliminate fees from your life! Have you ever accidently written checks for more than is in your checking account? At my bank they charge $35 per check overdraft. Here are two overdrafts the same day, followed by another $35 fee if the account remains overdrawn for more than 5 days. Don’t let this happen. Here’s a tip that can help.

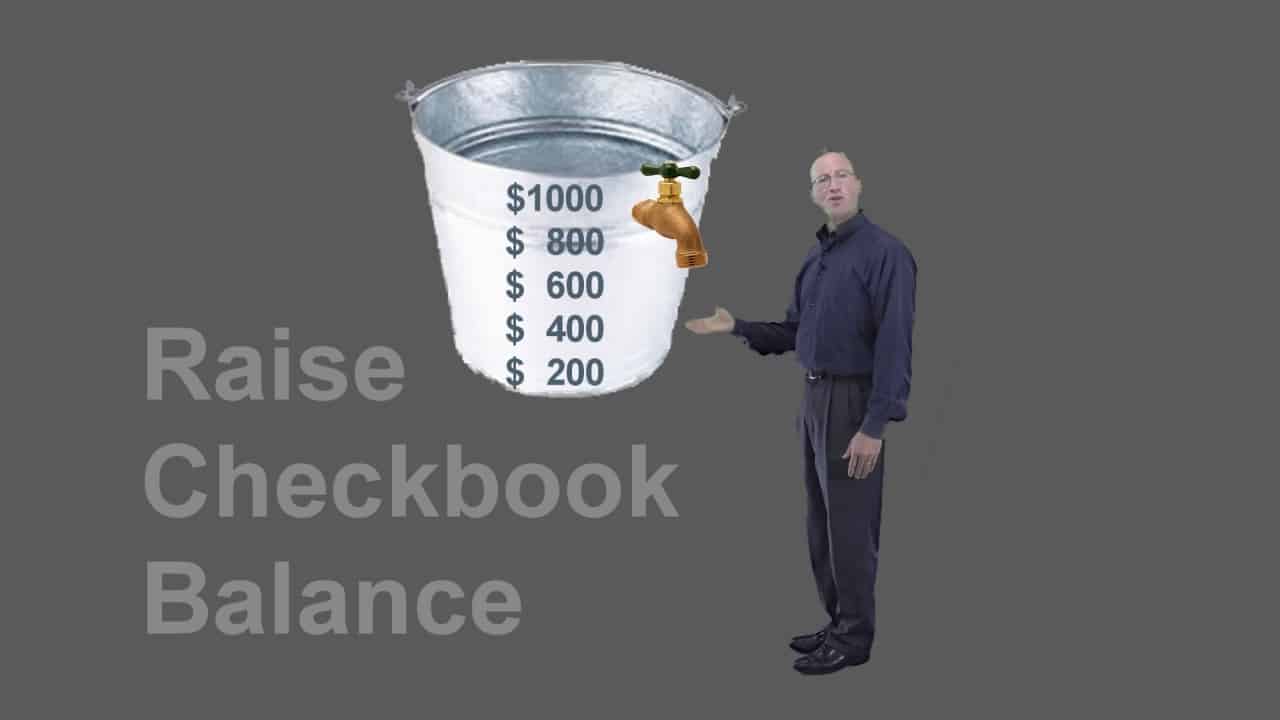

Use the first money you save to raise your checkbook balance (maybe so it never goes below $1000). But it is a buffer. IT IS NOT FOR SPENDING, it’s simple insurance against overdraft fees.

Here’s another tip. Whenever you get assessed a fee, from anybody (bank, credit card, whatever) always call them and plead your case. These overdrafts are real, but I called and they reversed them. Some banks won’t offer this to you unless you specifically ask them to waive the fees! It usually works if you don’t abuse it. So, always call and ask.

Also, pay off all bad debt before you start investing for the future. One of my first videos was about the Miracle of Compound Interest, but penalty fees and expensive interest rates cause this amazing miracle to work against you, instead of for you.

A typical credit card purchase takes 10 to 20 years to pay off if you only pay the minimum monthly payment. Worse, if you miss a payment on any other loan or credit card, then your interest rate will typically jump from something like 18% to something like 29%. And every 2 or 3 years you’ll owe twice as much!

Fees and expensive interest rates are like leaks to your precious savings and steal from your tomorrow. You must stop these leaks.

Always pay your credit card balance on-time and in-full. This is the most common example of bad debt. The interest rates are very high, so avoid them by paying the total amount due, and on-time. Even with the speed of the internet, banks sometimes require a surprising 3 to 5 business days to complete these payments. So don’t cut it close. Stay a week ahead.

Student loans and home mortgages might (not necessarily, but might) be examples of good debt, but recall that servicing these loans must fit into your budget.

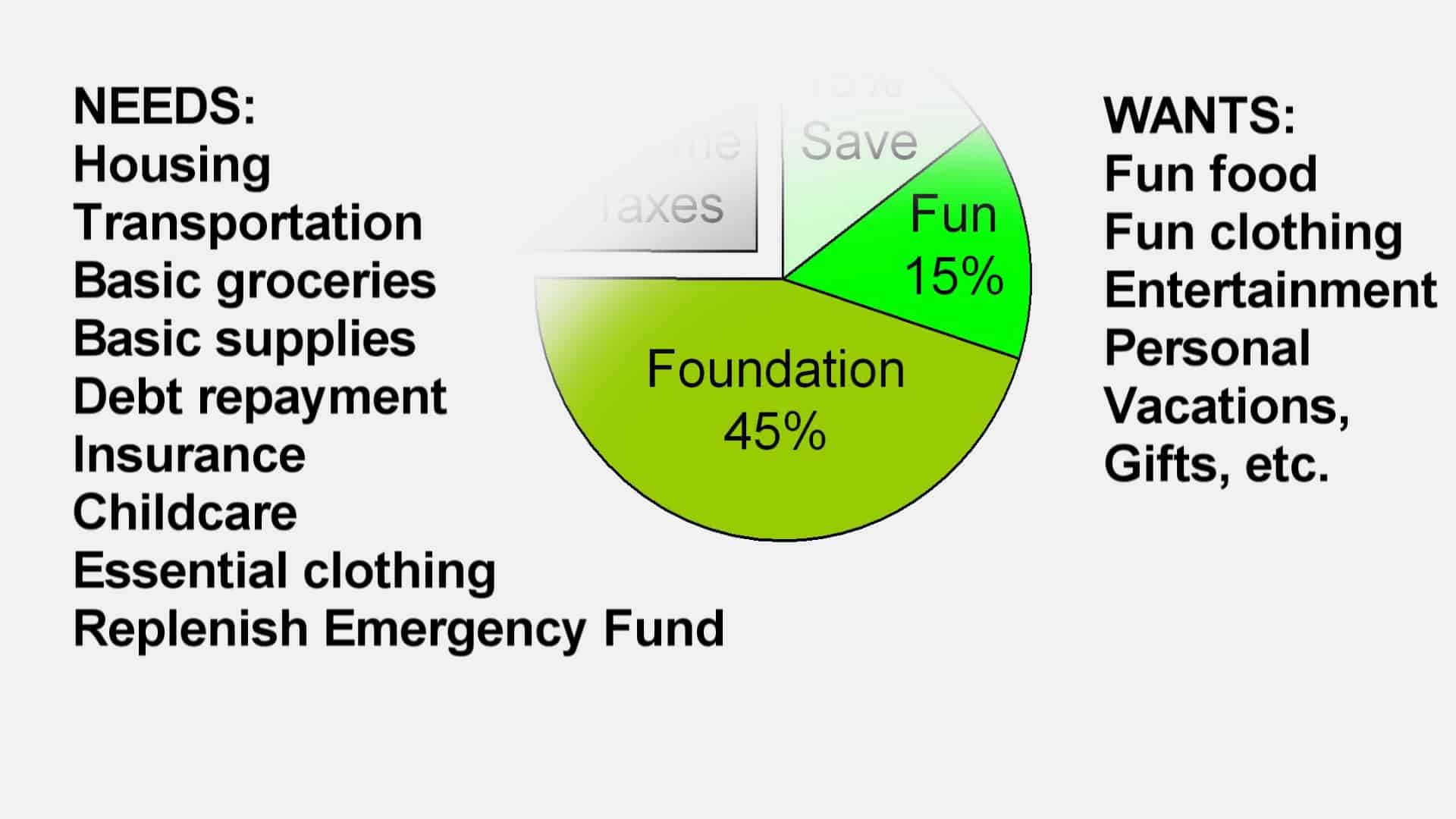

As you know, stuff happens. Remember earlier I suggested three questions to help you identify those MUST, or Foundation expenses? You will need money to pay for those if you were to lose your job. That’s why many advisors recommend a 6-month reserve. A money market account is perfect for this. Figure out what is right for you, but do something.

Buy the insurance you need. Most need health, auto, and homeowners or renters insurance. Buy life insurance only if you have dependents. These might be the types of insurance you might WANT to buy.

There are other types of insurance that “you are sold”.

You are almost always better off buying Term insurance than paying more for Whole, Universal, or Variable Life Insurance products which combine insurance with some investment attributes. Then, invest or pay off your mortgage with the difference.

With all that in place you can now safely begin investing your savings towards your big-ticket items and retirement.

Find other explanatory videos, smart tips, and links to useful resources at FinancingLife.org.

Footnotes and Credits:

The opening/closing music “Because” is by David Modica from his Stillness and Movement album, published and licensed by Magnatune.com .

The closing photo “Trees in the Fog” is by Yann Richard under the terms of the Creative Commons BY 2.5 license.

This video may be freely shared under the terms of this Creative Commons License BY-NC-SA 3.0.

————————————————————————–

What’s your learning style? Would you prefer a book?

- to learn at your own pace?

- to mark with notes?

- to use as reference?

- to give as a gift?

- or, even just to support this non-profit educational website (thanks!)

Take a closer look at the paperback book.

| Common Sense Investing: Ten Simple Rules to Finance Your Dreams

|